Sale of a residential house is taxable under the Income Tax Act. When you sell a house, you are required to pay capital gain tax on the profit received from the sale. The Income Tax Act,1961 provides relief from tax payment in such a case under Section 54 , subject to fulfilment of certain conditions. Let’s analyze, what does section 54 talk about and how we can apply it to save tax.

Here we go:

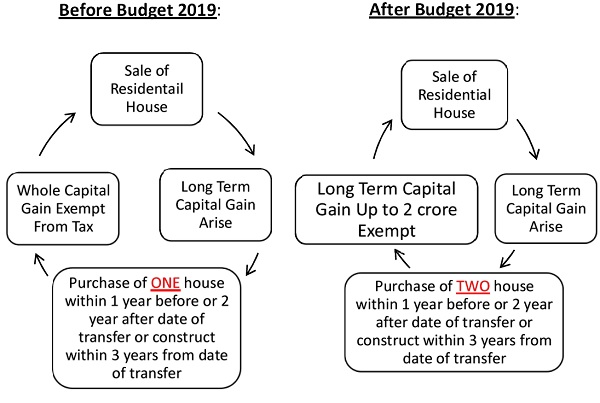

ithin 3FOR YOUR KIND ATTENTION:

W.e.f. A.Y. 2020-21, an individual or HUF can claim exemption for investment house (i.e., can purchase or construct 2 house). This exemption ids available only if long term capital gain is upto Rs. 2 crores.

Points to be noted before we proceed:

2. In case of compulsory acquisition, the period for purchase/ construction of new house will start from the date of receipt of compensation.

3. If exemption for investment in 2 houses is availed of, then this exemption cannot be availed again for the same or any other assessment year.

4. The new house must not be sold before completion of 3 years.

What if the new house is transferred/sold before 3 years complete?

The exemption claimed earlier shall stand withdrawn. Means, while calculating the capital gain on the sale of this new house, the exemption claimed earlier will be deducted from the cost of acquisition of new house.

So, if the 4 conditions mentioned above are satisfied, then you can claim capital gain exemption. But, HOW MUCH?

Lower of :

Amount of Capital gain vs Amount invested in purchase/ construction of new house

* Amount invested also includes the amount of capital gain which is unutilised and deposited in Capital Gain Deposit Account Scheme on or before the due date of filing return of income. Means you can claim exemption for deposited amount also. You can use the deposited amount within 2 or 3 years as mentioned in the section for purchase or construction of the house.

What if the amount deposited is not utilized for purchase/construction of new house?

The amount unutilised and already claimed as exemption will be taxed as long term capital gain for the year in which the period of 2 or 3 years expires.

Let’s analyze Sec.54 with some basic questions –

Q 1. What should be the period of holding of house property to consider it as Long term capital asset?

– 24 months

Q 2. Can a person other than an Individual / HUF claim such exemption?

– No

Q 3. An Individual sold a shop owned by him and purchased a new house. Can he claim exemption on capital gain u/s 54?

– No, asset sold must be a residential house.

Q 4. An Individual sold a house and purchased a plot of land. Then he constructed a house on it. Can he claim exemption on capital gain u/s 54?

– Yes, because it’s construction of residential house.

Q 5. An individual sold a residential house owned by him and purchased a shop. Can he claim exemption on capital gain u/s 54?

– No, asset purchased/constructed must be a residential house.

Q 6. An individual sold a residential house owned by him and purchased 2 houses in the previous year 2019-20. Capital gain amounted to ₹3 crores. Can he claim exemption on capital gain u/s 54?

– No, because the amount of capital gain exceeds ₹2 crores. Exemption for investment in 2 houses is available only if capital gain is up to ₹2 crores.

Q 7. An individual sold a residential house owned by him. Capital gain amounted to Rs. 5 lakhs. He deposited Rs. 5 lakhs in the Capital Gain Deposit Account Scheme as he was not able to utilize it for purchase/construction of residential house before the due date of filing return of income and claimed exemption u/s 54. Next year, he withdrew the money to purchase some gold. Will the exemption granted be revoked on purchase of gold from the money withdrawn from the scheme?

– Yes, exemption will be revoked and the exemption granted earlier will be charged to tax as long-term capital gain because of the fact that the withdrawn money was utilized for purchase of asset other than residential house.

Q 8. Can an individual/HUF claim capital gain exemption on purchase or construction of a residential house outside India?

– No, the house purchased or constructed must be situated in India.

Need any assistance than

No comments:

Post a Comment